.svg)

Why VCs Reject Foreign Corporations: How Jurisdiction Choice Kills Fundraising Before It Starts

- CategoryEntrepreneur

- DateMarch 8, 2026

- Share

You’ve built traction, aligned product‑market fit, and you know your numbers. You pitch confidently, but the conversation quickly shifts when investors see your corporate structure: a foreign company in an unfamiliar jurisdiction.

Suddenly the valuation slides, questions multiply, and the deal that looked solid just a few slides ago starts to fall apart. This scenario is not uncommon in 2026, and it often comes down to something founders overlook: investor expectations around jurisdiction and corporate structure.

Venture capital firms aren’t just buying into your technology, they’re buying into your legal and operational foundation. What looks neutral or advantageous as a founder can read as risk, friction, or uncertainty to an investor.

Why Jurisdiction Choice Matters to Investors

When a VC evaluates a startup, they don’t just assess the business model and team. They evaluate legal certainty, ease of future rounds, liquidity events, and exit pathways. Jurisdiction plays into all of these factors.

Investors typically prefer entities formed in jurisdictions with well‑established corporate law, strong shareholder protections, predictable legal systems, and reliable enforcement mechanisms. These jurisdictions provide a clear runway from seed to Series A, through acquisition or IPO.

When a company is incorporated in a jurisdiction with ambiguous legal precedents, weaker shareholder rights, or unpredictable enforcement, investors see higher transaction costs, structural inefficiencies, and greater execution risk.

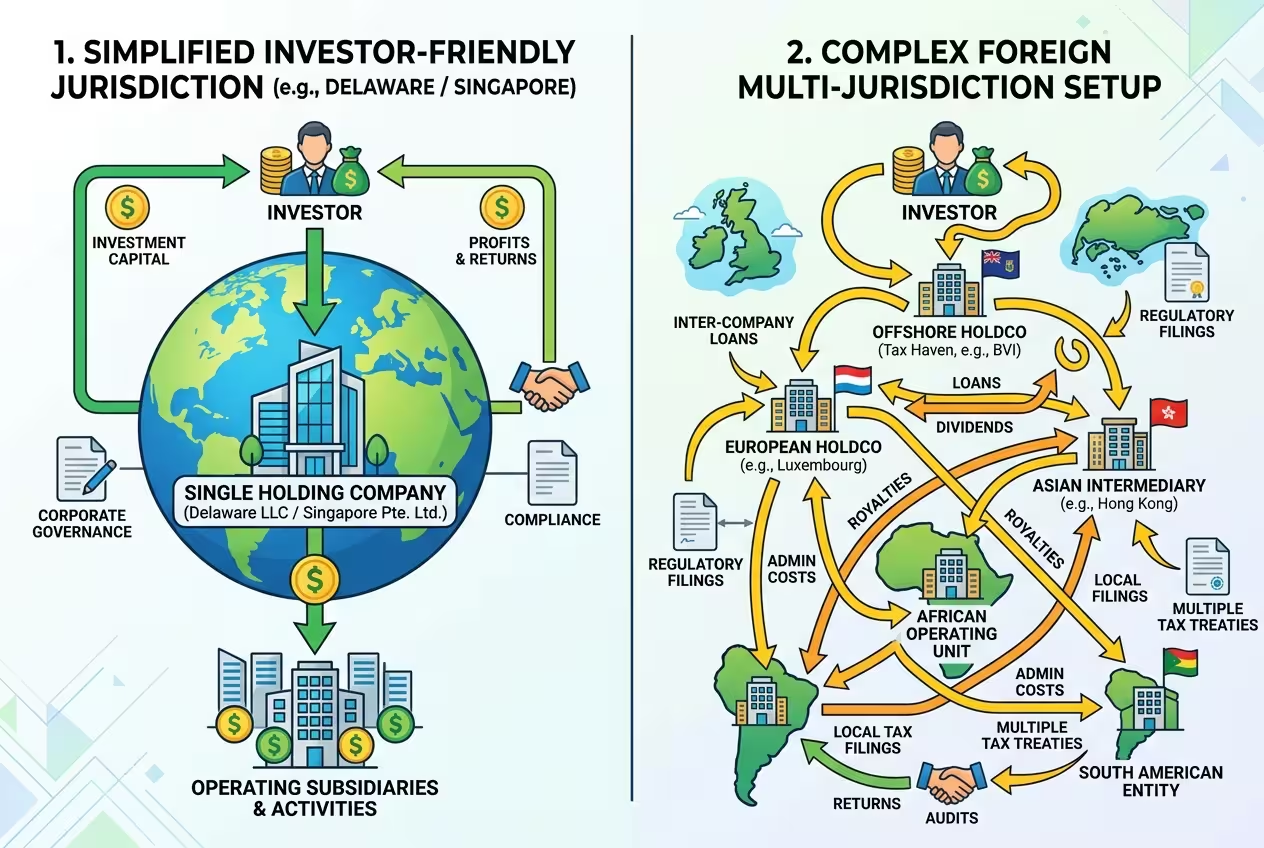

The Familiarity Factor: Delaware and Singapore

Certain jurisdictions have become de facto standards in the VC world. In the US, Delaware C‑Corporations remain the most recognized structure for institutional investment. Delaware corporate law provides:

- Robust body of case law for shareholder rights

- Predictable legal outcomes and tailored corporate governance

- Well‑understood mechanics for equity, liquidation preference, and investor protections

In Asia, Singapore has emerged as another favored base for venture capital because of its strong legal framework, double taxation treaties, and regional credibility. Both Delaware and Singapore have systems investors trust without reservation.

When a company is incorporated in one of these jurisdictions, investors can model their risk, negotiate term sheets with confidence, and structure future exit strategies with clarity.

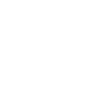

Empty Legal Precedent and Perceived Risk

When companies are incorporated in less standard jurisdictions, small offshore centers, emerging markets with developing legal systems, or regions without well‑paid corporate law specialists, investors cannot easily model outcomes.

They ask questions like:

- How are shareholder disputes resolved here?

- What legal precedent exists for protective provisions?

- Can preferred stock terms be enforced predictably?

- How will future rounds affect governance?

These are not hypothetical questions in investors’ minds, they influence investment readiness. Uncertainty in any of these areas often leads to deferred investment or outright rejection.

Tax Treaties and Cross‑Border Efficiency

Many investors think beyond the initial check, they think about future participation in global markets, potential listings, and cross‑border liquidity. Tax treaty networks play a significant role in these projections.

Companies formed in jurisdictions with limited tax treaties can face double taxation, inefficient revenue repatriation, and obstacles during acquisition structuring or cross‑border operations. Founders may overlook this, but experienced investors consider it a structural risk.

A well‑connected tax treaty network simplifies future growth and reduces friction for multinational operations, or at least that is the investor’s expectation.

Contract Enforceability and Judicial Certainty

In venture capital, contracts are how risk is governed and mitigated. Founders often think the product, team, or traction is the compelling factor, but investors are equally focused on how enforceable agreements are across jurisdictions.

If a legal system is understaffed, lacks corporate expertise, or has ambiguous enforcement mechanisms, investors anticipate friction. Contract certainty is not merely academic; it influences real outcomes in board disputes, liquidation scenarios, merger integrations, and more.

Investors prefer legal environments where judicial certainty is backed by tangible track records and deep corporate law scholarship.

Equity Structures and Shareholder Rights

Complex equity structures are common in early‑stage businesses, founders retain control while offering preferred terms to early investors. These structures depend on legal frameworks that support:

- Convertible preferred shares

- Protective provisions

- Liquidation rights

- Drag‑along and tag‑along rights

Certain jurisdictions simply don’t support these mechanisms in the same way, or their legal infrastructure makes enforcement uncertain or protracted. For VCs, this translates into structural risk that may outweigh upside potential.

Perceived Exit Challenges

When investors evaluate a deal, they plan the exit as early as the first round. If a startup is domiciled in a jurisdiction with limited exit precedents, investor interest can cool.

The logic is pragmatic: buyers, especially large public companies or global strategics, may prefer acquiring a business based in a familiar legal regime. Limited exit pathways make the investment thesis harder to justify.

Delaware, Singapore, and well‑established EU jurisdictions often have clearer exit histories and broader acquirers’ familiarity. This historical confidence plays into how investors assess upside scenarios.

Real Consequences: Deals Slipping Through Fingers

In 2026 it is increasingly common for founders to receive feedback like:

“We love the team, technology, and traction, but we can’t invest in your current structure.”

This kind of statement has little to do with your business fundamentals. Instead, it reflects structural friction, an invisible obstacle that kills deals early, long before term sheets or valuation debates even start.

Being unaware of these investor preferences leaves founders vulnerable to repeated “almost” conversations: those that look promising until the term sheet stage and then quietly fade.

How to Align Your Structure With Investor Expectations

Understanding investor expectations is one thing; acting on them is another. Smart founders treat their corporate structure as a part of their fundraising strategy. This isn’t just about incorporation; it’s about:

- choosing a jurisdiction that investors trust

- documenting corporate governance correctly from the start

- aligning equity structures with institutional preferences

- thinking ahead to Series A and exit scenarios

These considerations do not belong at the end of your checklist, they belong at the beginning. Structuring your company for investor readiness creates credibility and reduces friction when you actually enter the market.

Beyond Jurisdiction: Substance, Transparency, and Trust

While jurisdiction matters, another layer that investors watch closely is substance. A company with shell incorporation in one location but team, revenue, and operations elsewhere signals risk. Investors are increasingly requiring evidence of:

- demonstrable operational presence

- aligned leadership and decision‑making locations

- transparent reporting and compliance readiness

Investors are not simply risk‑averse; they are structured to protect limited partners’ capital and ensure predictable outcomes. Clear substance reduces uncertainty and makes your business easier to support structurally.

Make Structure a Strategic Advantage

Jurisdiction choice is more than a legal detail, it is a signal to investors about your understanding of global markets, future exit pathways, and risk management. Founders who dismiss structure as a technicality often find their fundraising narratives derailed before they ever get traction.

Instead, treat corporate structure as an integral part of your pitch strategy. When investors see a company incorporated in a trusted jurisdiction, with proper governance, predictable legal frameworks, and a credible equity structure, your narrative becomes easier to champion, not harder.

If you want to align your corporate setup with investor expectations and remove structural barriers from your fundraising story, it’s worth examining your current jurisdiction, equity arrangements, and strategic outlook early in the process. Thinking this way not only improves your chances of investment interest, it makes your business fundamentally more resilient and investor‑ready in 2026 and beyond.